| 169 Raceview Drive, Ona, WV 25545 | tlheadley@hedleycompany.com | 681.356.1776

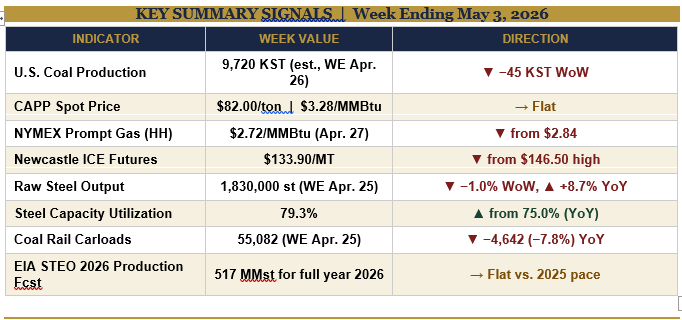

KEY SUMMARY SIGNALS | Week Ending May 3, 2026

EXECUTIVE SUMMARY

CHARLESTON, W.Va. — The week ending May 3, 2026, finds the U.S. coal industry in a position it rarely gets credit for occupying: strategically indispensable and operationally sound, even as the numbers show the seasonal softening that EIA has been forecasting all spring. Production continues on its established pace, steel output is posting multi-year highs on the back of robust met coal demand, and the international market — driven squarely by the U.S.-Israeli military campaign against Iran and the effective closure of the Strait of Hormuz — has locked in a structural war premium that shows no sign of vanishing regardless of diplomatic noise.

The headline regulatory story of the week is EPA’s April 17 proposed rule revising Coal Combustion Residuals (CCR) disposal regulations — a direct-cost relief measure for operating and legacy coal plants. The public comment window runs through June 12, with a virtual hearing on May 28. Meanwhile, DOE Secretary Wright’s April 30 deadline for a final FERC co-location rule has arrived: that rule, if executed properly, creates the legal framework for data center loads to co-locate directly at coal-fired generation sites, converting baseload coal plants into preferred anchor infrastructure for AI compute demand.

On the market side: CAPP spot holds at $82/ton — no near-term catalyst for domestic thermal price improvement while Henry Hub lingers near $2.72/MMBtu and spring shoulder conditions build utility stockpiles at approximately 3 MMst/month. The more interesting price story is Newcastle at $133.90/MT — down from the March 20 high of $146.50 but still nearly 9% above pre-war levels, with Asia and Europe both accelerating coal procurement as their LNG pipelines face Hormuz disruptions. The war premium is embedded; what moves next is how long it holds.

AAR Week 16 coal carloads came in at 55,082, a year-over-year decline of 4,642 (−7.8%). That number requires interpretation, not panic: the comparison week in 2025 was the period when coal carloads ran 59,726 — an unusually strong reading tied to late-spring utility restocking. The underlying story this year is mild weather, building stockpiles, and lower coal-fired generation — all of which EIA has been forecasting since the April STEO. The 52-week trend and export rail volumes tell a different story, and the met coal rail flow supporting record steel output is a countervailing positive.