COAL CURRENTS WEEKLY INTELLIGENCE FOR THE U.S. COAL INDUSTRY

A Publication of The Hedley Company | CHARLESTON, W.Va. | VOL. 2, NO. 20

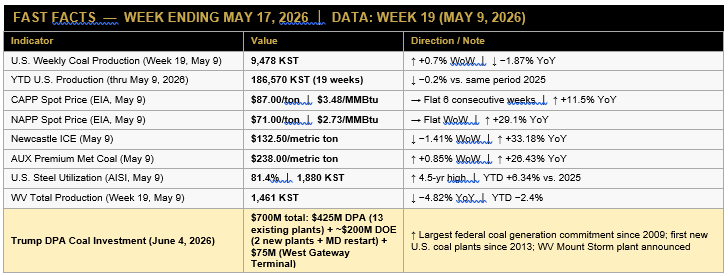

FAST FACTS — WEEK ENDING MAY 17, 2026

EXECUTIVE SUMMARY

CHARLESTON, W.Va. — U.S. coal production for the week ending May 9 (Week 19) came in at 9,478 thousand short tons (KST), up 63 KST from the prior week (+0.67% WoW) but down 1.87% against the corresponding week in 2025. Through nineteen weeks of 2026, total U.S. production stands at 186,570 KST — a negligible 0.2% below last year’s pace, a far better outcome than EIA’s May STEO forecast of a 10-million-short-ton full-year decline would suggest. The national number conceals a stark regional split: Wyoming is running 4.4% ahead of 2025 YTD at 75,038 KST, the Western region as a whole is up 2.4%, and Utah has posted an extraordinary +20.6% YTD gain. Appalachia, by contrast, is clinging to near-parity at -0.6% YTD, with West Virginia down 2.4% and WV CAPP off 3.5% — while the Interior region is in structural decline at -7.4% YTD, led by Illinois at -12.0%.

Pricing this week tells an equally divided story. Central Appalachian coal has been locked at $87.00/ton for six consecutive weeks — $3.48/MMBtu on a heat-adjusted basis — while Henry Hub spot gas sits at $2.88/MMBtu. That $0.60/MMBtu spread puts CAPP coal above gas at the margin, a headwind for domestic dispatch economics. But PRB coal at $15.60/ton ($0.89/MMBtu) and ILB at $56.75/ton ($2.40/MMBtu) remain decisively below gas at the wellhead, keeping dispatch economics favorable across the Western and Interior regions. Internationally, the picture is dramatically more favorable: Newcastle thermal coal settled at $132.50/metric ton (+33.18% YoY), and Australian premium hard coking coal reached $238.00/MT (+26.43% YoY) — both benchmarks reflecting a global energy security rerating driven by the Strait of Hormuz closure and its continuing ripple effects through LNG supply chains.

The unambiguous bright spot remains U.S. steel. AISI reported raw steel production of 1,880 KST for the week ending May 9, a capability utilization rate of 81.4% — the highest in 4.5 years — and YTD output running 6.34% above 2025. Metallurgical coal demand is structurally supported. Rail performance, however, is a mixed signal: Norfolk Southern is consistently failing to meet its planned coal loadings in Appalachia, running 12-14% below plan in recent weeks. CSX is performing near plan. Both railroads showed total Appalachian coal loading plans of approximately 11,500 combined carloads per week — with NS accounting for a meaningful shortfall. River barge operations are steady, with West Virginia loading 392 barges in Week 19.

The week’s most consequential development arrived as this issue was going to press: on June 4, President Trump invoked the Defense Production Act of 1950 to direct nearly $700 million in federal support to U.S. coal-fired generation infrastructure. The package is the largest single federal commitment to coal generation capacity since the Obama-era ARRA spending on clean coal research in 2009 — and the first DPA invocation specifically targeting coal plant operations. The $425 million in DPA funds is directed to 13 existing coal-fired power plants across ten states — West Virginia, Kentucky, North Carolina, Indiana, Tennessee, Arkansas, Arizona, Oklahoma, North Dakota, and Wisconsin — for upgrades designed to extend operational lives by decades. Duke Energy, Hallador Energy, and Oklahoma Gas and Electric are among the identified beneficiaries.

Accompanying the DPA action, the DOE is directing approximately $200 million in grant funding to build two new coal plants — the first new U.S. coal-fired generation since 2013 — in Alaska and at Mount Storm, West Virginia (pursued by TerraPurus Inc.), and to restart the AES Warrior Run generating station near Cumberland, Maryland. Private matching funds bring total capitalization of those projects to approximately $386 million. Mount Storm sits squarely in Northern Appalachian territory; a new plant there is a direct, long-term demand signal for WV NAPP production. Additionally, $75 million in DPA funding breaks ground on the long-stalled West Gateway Terminal in Oakland, California — a coal export facility 20 years in the making, projected to reach full operations by summer 2028. That terminal’s 12-million-ton annual capacity creates a Pacific Basin export channel for Wyoming, Montana, and Utah producers that has not existed in any meaningful operational sense. The administration projects 14,000+ jobs supported across coal, construction, rail, and maritime sectors and an estimated $50 billion in reduced generation costs to consumers. The full implications of this announcement — for plant operators in the ten covered states, for Western producers eyeing the Oakland terminal, and for the legal architecture protecting coal capacity under the DPA — are analyzed in Sections 7 and 9 below. For more, please subscribe…