COAL CURRENTS: WEEKLY INTELLIGENCE FOR THE U.S. COAL INDUSTRY

A Publication of The Hedley Company | VOL. 2, NO. 21 | Week Ending May 24, 2026

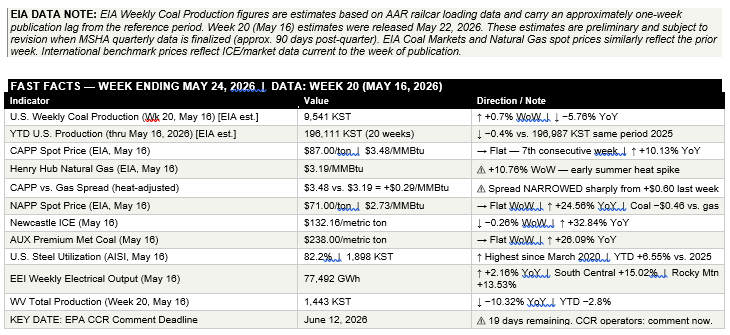

FAST FACTS

EXECUTIVE SUMMARY

CHARLESTON, W.Va. — The week ending May 24 delivers a data set more energized than the prior six weeks of spring shoulder-season flatness — for a reason that reshapes the price analysis across every coal basin: an early summer heat event arrived in the South Central and Rocky Mountain regions with enough force to push Henry Hub natural gas spot prices from $2.88 to $3.19/MMBtu in a single week (+10.76%), while simultaneously driving total U.S. electrical output to 77,492 GWh — the highest weekly figure in the six-week tracking period. South Central output posted a +15.02% YoY gain; Rocky Mountain gained 13.53%. Summer arrived early in the south-central grid, and it is burning gas at a rate that matters for every coal dispatch decision in basins competitive with gas at current prices.

That gas price move reshapes the CAPP dispatch arithmetic materially. Seven consecutive weeks at $87.00/ton ($3.48/MMBtu) put CAPP coal at $0.60 above Henry Hub as recently as last week. This week, with Henry Hub at $3.19, that premium narrows to $0.29/MMBtu — a 52% reduction in the gas advantage in a single data point. NAPP at $2.73/MMBtu is now $0.46 below gas, an advantage that doubled in one week. ILB at $2.40 holds a $0.79 advantage. PRB’s dominance is absolute at $0.86/MMBtu. If Henry Hub holds above $3.00 through a warm summer — consistent with EIA’s Q3 CDD forecast of +8% vs. last year — the CAPP dispatch calculus shifts from structurally disadvantaged to competitive at the margin.

Production at 9,541 KST for Week 20 is the EIA estimate released May 22 — the third consecutive week of recovery from the Week 16 low of 9,401 KST. But the YoY comparison turned sharply negative at −5.76%, against a strong corresponding week in 2025. YTD through twenty weeks, estimated U.S. production stands at 196,111 KST, −0.4% behind 2025’s 196,987 KST through the same point. The deficit has grown modestly from last week’s −0.2%.

West Virginia delivered the week’s most jarring single data point: WV CAPP at 634 KST, down 17.77% from the corresponding 2025 week. WV NAPP at 809 KST held closer to prior-year levels (−3.46%). Combined WV total of 1,443 KST was down 10.32% YoY — the steepest weekly YoY decline in the state’s six-week tracking period. A single-week decline of this magnitude in CAPP underground production can reflect operational factors — equipment cycling, mine sequencing, shift scheduling — as readily as structural market withdrawal. The YTD WV CAPP figure of −4.2% is the more durable signal. Monitor the next two weeks.

Steel production at 1,898 KST and 82.2% utilization holds at its highest since March 2020 for the second consecutive week. Great Lakes district at 533 KST is the demand center for Northern Appalachian coking coal. Australian premium hard coking coal at $238/MT confirms the global market is pricing met coal demand at levels that validate Appalachian underground mine investment.

On transportation: CSX ran essentially on plan in Week 20 — 9,722 actual versus 9,725 planned, near-perfect execution. Norfolk Southern’s Central Appalachian shortfall persisted: 500 actual versus 590 planned (−15.3%). NS NAPP finally reached plan at 440/440. The NS total of 940 versus 1,030 planned (−8.7%) is a modest improvement from recent weeks but remains a systematic underperformance that NS-served shippers should be documenting for the STB record.

Two regulatory deadlines arrive within days of each other: EPA CCR public hearing May 28 and Senate Whitehouse MATS investigation responses also due May 28. The EPA CCR comment deadline closes June 12 — nineteen days from this report. The DOE’s fifth emergency order keeping J.H. Campbell running through August 18 was issued this past week. The D.C. Circuit has the case. Watch the litigation; its outcome defines whether Section 202(c) becomes a durable coal fleet preservation instrument or a one-time emergency tool.