| 169 Raceview Drive, Ona, WV 25545 | tlheadley@hedleycompany.com | 681.356.1776

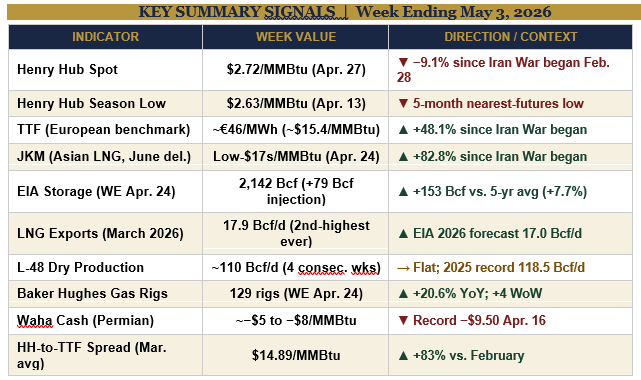

KEY SUMMARY SIGNALS | Week Ending May 3, 2026

EXECUTIVE SUMMARY

CHARLESTON, W.Va. — The natural gas market entering May 2026 is split clean down the middle: a domestic market drowning in supply, and a global market on fire. Henry Hub at $2.72/MMBtu and Waha cash bouncing between −$5 and −$8/MMBtu tell one story. TTF at ~€46/MWh and JKM in the low-$17s/MMBtu tell another. The U.S.-Israeli military campaign against Iran, now in its 10th week, effectively closed the Strait of Hormuz to LNG tanker traffic on February 28. It has not reopened in any meaningful way. That single fact has driven TTF up 48.1% and JKM up 82.8% since the war began, while Henry Hub has declined 9.1% over the same period, producing the widest sustained U.S.-to-global gas price spread in modern LNG market history.

The storage picture is comfortable. EIA confirmed 2,142 Bcf working gas as of April 24 — 153 Bcf above the 5-year average and 116 Bcf above last year at this time. The injection of 79 Bcf for the week ending April 24 exceeded the 5-year average of 63 Bcf, though below the 105 Bcf injection in the same week of 2025. EIA projects 2.125 trillion cubic feet in net injections for the full 2026 season — 9% above the 5-year average — ending October at approximately 4,015 Bcf. That surplus is the structural ceiling on Henry Hub prices through mid-year.

The headline of the week: Golden Pass LNG shipped its first cargo on April 22, 2026 — becoming the 9th U.S. LNG export terminal. The QatarEnergy/ExxonMobil facility near Port Arthur, Texas arrives at the most commercially favorable moment in U.S. LNG history. The Henry Hub-to-TTF spread averaged $14.89/MMBtu in March. Golden Pass Train 2 is expected late summer 2026, Train 3 in early 2027; the full 2.0 Bcf/d nominal facility will be one of the three largest U.S. terminals when complete.

Production holds at approximately 110 Bcf/d for four consecutive weeks — spring maintenance and shoulder-season curtailments masking the underlying growth trend EIA projects to carry full-year output to 120.8 Bcf/d. Baker Hughes gas-directed rigs hit 129 for the week ending April 24, +20.6% year-over-year. The supply response is real. The production story is intact. The price story is in the global spread, not the Henry Hub number.